1723

The numbers will determine your fate

(lemmy.world)

A place to share screenshots of Microblog posts, whether from Mastodon, tumblr, ~~Twitter~~ X, KBin, Threads or elsewhere.

Created as an evolution of White People Twitter and other tweet-capture subreddits.

Rules:

Related communities:

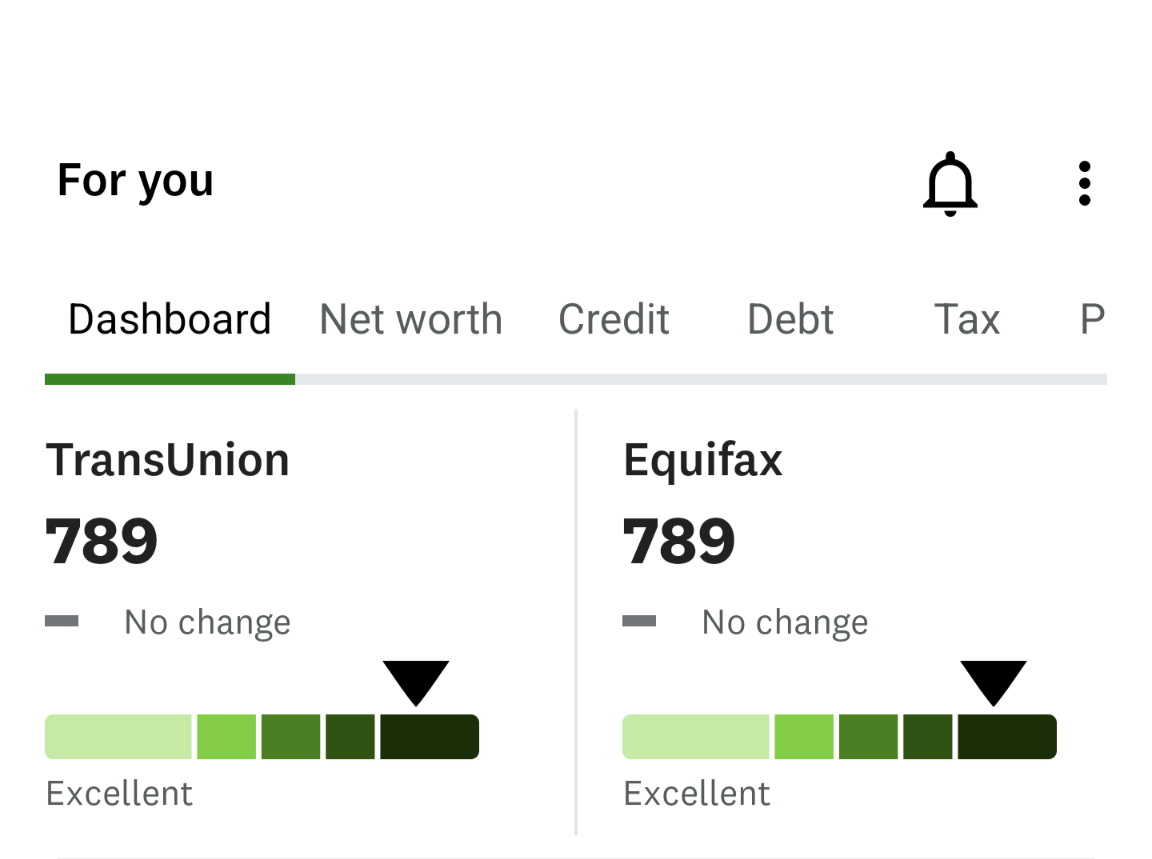

You don't have to be in debt, but you do need open credit lines. Having debt on them actually makes your score worse.

Her score likely went down because she closed out a credit line, i.e the open loan, so technically the "i have an open 5yr loan ive been paying on diligently" is no longer part of her score. The fact that she did pay it off is part of that score, but its weighted differently.

If she instead had 40k of credit cards she had open for 5yrs, with zero debt on them, her score would have gone up. Just having the account open, even not using them, shows a high "credit to debt usage" ratio and "a long time open loan." Both of those make up about 45% of your "credit score."

So no, you dont have to use a CC every month to keep a high credit score. If you want a high score, you want to open a credit card or 2 for their max value until you get about 30k-40k of total credit, and then don't use them at all. Not a bit. Never close them. The "long time accounts" + "high amount of debt not in use" + "never delinquent" is roughly 80% of your score. You can sail into the 700s/800s if you dont have any other credit hit.

I don't know why this dude is getting downvoted. This is basically what I do. And I have a great score.

Yeah I dug into all this a while back while I was trying to raise my score. Turns out the most productive thing I did was just ask my current cards to up my limit. A couple of them doubled, so it dropped my utilization way down, which shot my score way up. I think I was around 675 and went up to 750 just with that trick. I got into the 800s by paying off the credit cards.

Its an annoying metagame you have to play to get the "good interest rates," but those little tricks can save you a fuckton of money over time.

I think the point here though isn’t as much ‘how do we play the game?’ as it is why there hell are we all forced into playing a metagame that is so inherently harmful and specifically designed to encourage risky behavior (I.e. the idea of debt being favorable)?

It's a measure lenders use to figure out how likely they are to make money from loaning to you. It's a very successful metric for them. It's not really for your best interest, but if you're aware of what goes into it there are simple, harmless things you can do to raise your score and help you get better rates.

Because the alternative is "how white are you"