this post was submitted on 04 Mar 2024

1218 points (99.2% liked)

Comic Strips

12478 readers

3366 users here now

Comic Strips is a community for those who love comic stories.

The rules are simple:

- The post can be a single image, an image gallery, or a link to a specific comic hosted on another site (the author's website, for instance).

- The comic must be a complete story.

- If it is an external link, it must be to a specific story, not to the root of the site.

- You may post comics from others or your own.

- If you are posting a comic of your own, a maximum of one per week is allowed (I know, your comics are great, but this rule helps avoid spam).

- The comic can be in any language, but if it's not in English, OP must include an English translation in the post's 'body' field (note: you don't need to select a specific language when posting a comic).

- Politeness.

- Adult content is not allowed. This community aims to be fun for people of all ages.

Web of links

- [email protected]: "I use Arch btw"

- [email protected]: memes (you don't say!)

founded 1 year ago

MODERATORS

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

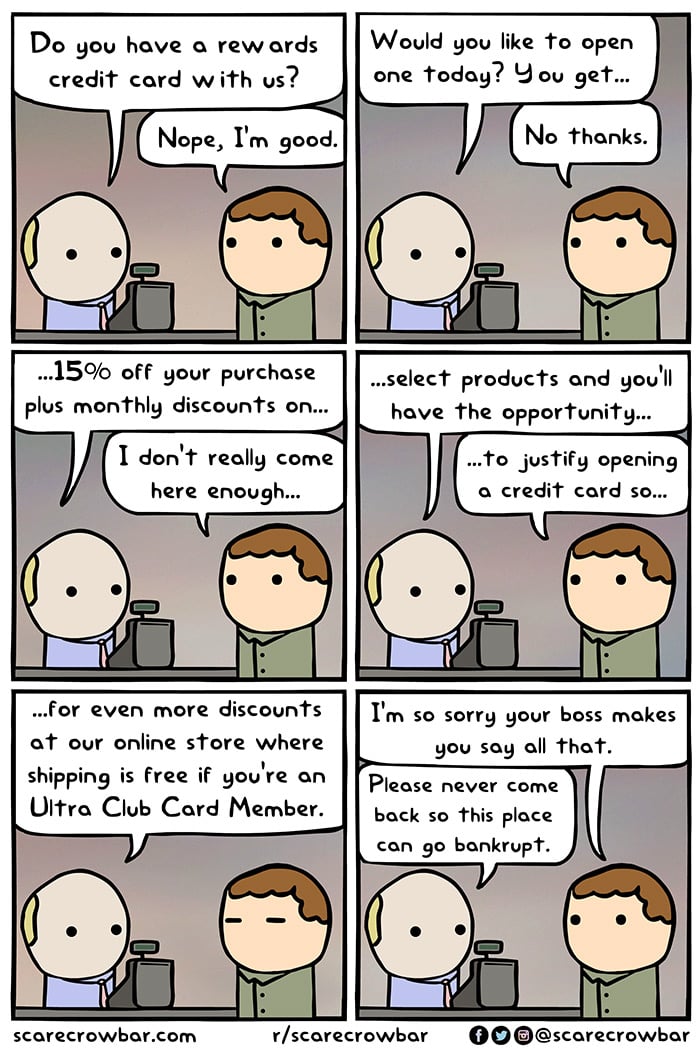

You aren't racking up enough interest on that card if you misplaced it. And they can surely see your buying history when you went to cancel and probably wouldn't waste the time with how wide a net they cast and how often people call to cancel afterwards.

The goal is to find the people easily addicted and get them full giving as much money as possible back to target. Anyone that gets a little here and there is good too but no reason to fight over them.

Sure, the occasional customer gets into a cycle for credit card debt and ends up paying big interest. That’s not where credit card companies make their money though. There’s a fee for the merchant to process each transaction, that’s the main revenue source. Then if we’re talking about a store card, they get the ability to track your purchases everywhere you use that card, and use that info to do better marketing, merchandising, and just generally get better at selling people stuff. It’s nice to make a buck when people buy things from your store, but it’s even nicer if you can make a buck when people shop elsewhere too.

The Credit Card Companies get their 2% fee but the banks get their interest rate. The average American owes > $6000 in Credit Card Debt. At your average usury rate of 20% that's $1200 every year for every American. That alot of fuckin money.

Friendly reminder that's all that a credit score is. Your profitability score.

Also not so friendly reminder they didn't exist until 1989 so every generation prior to you had a much easier time.

I think part of the problem is that just like reviews and scores the only acceptable range you can be within is the top <20%. And that range seems to be constantly shrinking. No one wants to eat at a restaurant with below 4 stars. No one wants to help people who aren't getting bigger and bigger loans making more and more interest.

We are a country that wants an unobtainable exceptionalism. Because that feels good and gives better returns. We focused entirely on the top and are squeezing harder to get more from it.

You get a chance to quantify and separate out by groups and it suddenly becomes a game to min-max people. It feels progressive but it just makes hierarchies.